Why SMEs are the future of export finance

SME EPC contractors may lack the scale and track record of the industry’s traditional heavyweights, but in emerging market infrastructure they are becoming too important for ECAs and lenders to ignore.

We hear a great deal about large ECA-backed infrastructure financings closed by the industry’s “big boys” — large international EPC contractors with strong balance sheets, established banking relationships and long track records in emerging markets.

Much less attention is paid to the smaller transactions led by mostly unknown names: small and mid-sized EPC contractors with annual revenues of up to €150 million, and often far less, that have limited experience executing projects in emerging markets and little or no experience with ECA-backed deals.

Yet these companies — the SMEs of the export finance market — represent the future of the industry.

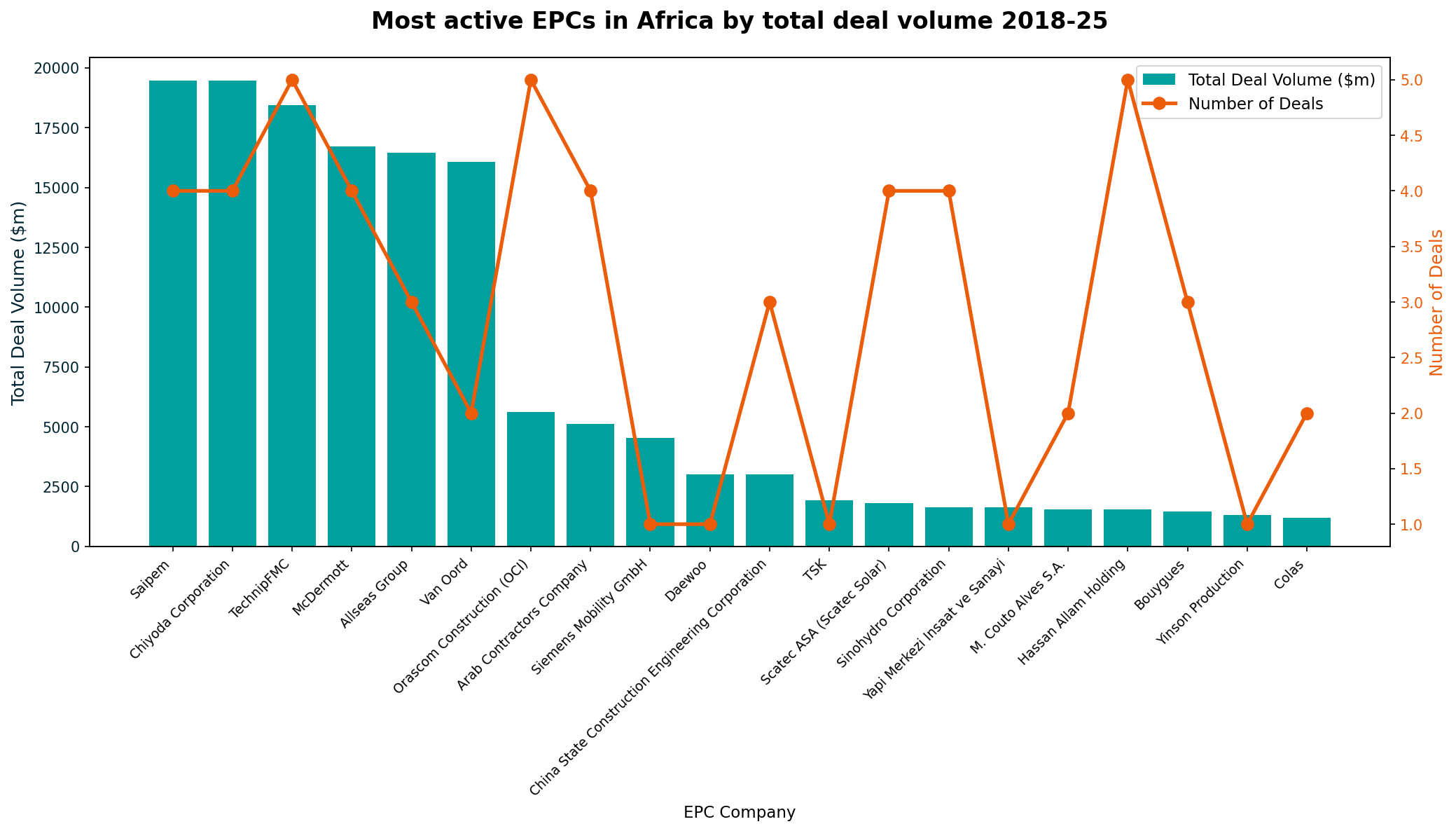

In today’s highly competitive environment, more ECAs are recognising that they cannot continue relying solely on the traditional roster of major exporters (see bar chart). If they want to remain relevant and expand their reach, they need to attract SMEs — whether national or international — that have genuine projects in hand and are looking for credible financing solutions.

Most of the deals we at Bluebird have helped close in Africa and other emerging markets over the past nine years — more than €2.3 billion in aggregate — have been led by SME EPC contractors, often on their first encounter with the ECA market. From transport and water to agriculture, these projects have shared one common feature: they were significantly more difficult than they may have appeared from the outside.

Arranging financing for a large and complex infrastructure project in a challenging emerging market is never straightforward. Doing so when the EPC contractor is an SME entering the ECA space for the first time is different again. Whether the project involves a road, railway, water supply system or agricultural infrastructure, the process is highly specific, unusually demanding and often far more fragile than comparable transactions led by established industry “heavy weights”.

It may look polished in conference discussions or LinkedIn posts, but the reality is very different. These transactions are typically full of daily obstacles, uncertainty, delays and years of effort before financial close — followed by further years of hard work during construction to ensure that the project is completed and the original promise is actually delivered.

A window of opportunity

There is today a genuine opportunity for SME EPC contractors in Africa and other emerging markets.

- The largest contractors are mostly focused on the biggest mandates. Their scale is an obvious strength, but it can also be a weakness. They are often heavy, slow-moving and, at times, too rigid in their approach. Sovereign borrowers do not always welcome that.

- Europe’s EPC base has been shrinking and has become increasingly selective about pursuing opportunities in emerging markets. In some countries, there are now very few domestic contractors still active in Africa.

- Chinese dominance in financed infrastructure projects across Africa has been receding, and that model carries its own structural weaknesses.

Taken together, these trends create real space for international SMEs to compete for meaningful projects — be it a €90 million road in Cameroon, a €200 million water project in Côte d’Ivoire or a €60 million agricultural project in East Africa. In many cases, these smaller contractors bring advantages that larger players do not. They are growth-oriented, hungry and willing to learn and far less likely to abandon a transaction once it becomes difficult.

Those qualities matter. Closing an ECA-backed sovereign deal in Africa requires resilience above all else. These projects involve countless moving parts, and many of the challenges that arise can kill a deal if they are not handled properly. It takes years of work to reach financial close, and contractors need to keep going through setbacks, delays and repeated restructuring. It is not a process for the faint-hearted.

But resilience, while essential, is not enough.

Enthusiasm is not a financing strategy

For SMEs, the challenge is not just to identify opportunities, but to approach them in the right way. The financing needs to be filtered early, structured carefully and prepared professionally long before the first serious engagement with lenders. If that does not happen, even a good underlying opportunity can lose credibility.

This is where smaller contractors often make avoidable mistakes. In their understandable desire to move quickly, they approach banks or ECAs too early — with immature ideas, structures that do not work, or ambitions that are simply not financeable. That does not just slow the process down; it can damage their reputation and reduce their chances of closing a transaction later.

If a contractor approaches a major lender seeking commercial ECA financing for a water project in an African sovereign market without understanding that the country can currently borrow only on concessional terms, it does not look serious.

If a company with annual turnover of €25 million asks a European ECA to support a €160 million project despite having no track record of delivering anything of that scale, the message is equally unconvincing.

The same applies when an exporter presents an ambitious content matrix and claims that certain equipment packages are “100% national content”, while overlooking the fact that they are being sourced through a very small trading entity and are not in fact manufactured in the ECA country at all. That is a clear red flag for any serious ECA, and rightly so.

These are not hypothetical examples. They are all situations we see in the market.

That is why financing strategy needs to begin from day one — and, in many cases, even before that, during the business development and marketing phase. Opportunities need to be filtered continuously, and once a serious one is identified, it must be shaped carefully and adjusted to the requirements of the relevant ECA and bank. Those requirements are not uniform. Each institution has its own nuances, and sometimes the differences are significant. The structuring work therefore has to be done in advance, before the approach is made.

Managing the SME risk profile

It is also important to acknowledge a more difficult reality: SMEs often carry higher performance risk in complex projects in emerging markets. They may have limited experience executing larger contracts, limited familiarity with difficult jurisdictions and little understanding of the mechanics of ECA financing. ECAs and banks are therefore right to be cautious.

The encouraging point, however, is that these risks can often be mitigated. That requires a carefully constructed execution plan, built with a long-term view and based on a realistic assessment of the contractor’s capabilities and weaknesses. It means identifying the likely pressure points in advance, understanding how those risks will be managed and, in some cases, sharing execution risk with another smaller contractor. The real discipline here is to look at the transaction without too much marketing language or wishful thinking. If the realities are assessed honestly, the problems can usually be addressed in a practical way.

In these projects, there are endless important decisions made at the outset that can determine whether a transaction ultimately succeeds or fails.

One of the most important is the choice of fronting ECA — and, where relevant, the reinsuring ECA. In theory, OECD-aligned ECAs should look broadly similar. In practice, they do not. There are major differences in national content policies, environmental and social requirements, openness to first-time contractors and internal approval processes. Those nuances can be significant and, at times, surprising.

If those distinctions are not understood properly from the start, precious time can be lost and the deal itself may be put at risk. And that is just one example among many.

The rule is simple: timing is everything. In most cases, there is a two- to three-year window in which to close a transaction of this kind, with dozens of key milestones along the way. If too much time is wasted at the beginning, the deal is often lost.

This is particularly true for large and complicated infrastructure projects in emerging markets, which already take years to bring to close. Banks and ECAs want to feel that they are dealing with someone who is bringing them a serious opportunity — one that is properly prepared, carefully structured and presented by someone who understands what he or she is talking about.

If SMEs genuinely use their natural advantages — agility, flexibility and a willingness to listen and learn — they are in a strong position to navigate this process successfully and, in some cases, to outperform much larger competitors. That applies not only up to financial close, but also during construction, when all of the promises made during the financing phase must be translated into delivery on the ground. We have seen enough successful examples to know that this is entirely achievable.

What ECAs and lenders need to do

At the same time, the ability of SMEs to succeed in this arena does not depend on them alone. ECAs and lenders also have an important role to play.

The bureaucracy and requirements applied to these transactions need to take account of the identity of the contractor and the reality of a first ECA-backed transaction being undertaken by an SME. That does not mean weakening core standards or compromising on fundamentals. But it does mean accepting that if ECAs genuinely want to attract such players, then the process — particularly for smaller deals — needs to become more pragmatic, proportionate and user-friendly.

There are several practical implications:

- SMEs need early visibility on likely lender requirements. They need to understand, from the beginning, the time commitment, advisory burden and cost implications of the process from initial engagement through to closing and construction. They cannot remain in the dark for too long. A €70,000 spend on an environmental and social report or a related requirement may be manageable for a multinational contractor, but for an SME it can be highly material.

- ECAs and banks need an embedded quick-screening mechanism that gives the SME a reasonably clear signal at the start as to whether the transaction has a realistic chance of ultimate approval. This is essential to avoid wasting time and money, and to prevent unpleasant surprises further down the line.

- There needs to be greater proportionality by deal size. A €40 million transaction should not be subjected to exactly the same approval process as a €120 million one. The level of review should be differentiated, and that should apply not only to environmental and social matters, but to the entire due diligence process.

- Financial institutes should enable more unique platforms for smaller buyer credit deals. Sometimes SMEs would start with a small “appetiser” deal of €15-20 million – which most European banks won’t be interested in, since it’s too small – and therefore unique funding platforms tailor-made for smaller deals are very necessary (there are several good ones in Europe, but still not enough). Obviously there are wide solutions for supplier credit and trade deals, but they don’t fit well the needs of infrastructure turnkey projects (even if they are small ones), therefore regarding small buyer credit deals - there is still a significant market gap.

Some ECAs and banks already have such mechanisms in place. Many still do not.

Competing for the SME market

An increasing number of ECAs and banks appear to understand that, in the context of infrastructure and social projects in emerging markets, the future of export finance may increasingly lie with SMEs. They also understand that competition over how to support and structure those deals is likely to intensify and in turn improve their offering.

That is already being reflected in the market:

- Some institutions are introducing greater flexibility around content sourcing definitions — a critical issue for EPC contractors, buyers and overall project pricing.

- Others are launching more attractive financing terms, including concessional routes that can be genuinely transformative.

- And some are moving towards a more pragmatic approach to environmental and social due diligence — an area that now has an outsized effect on EPCs, borrowers and the overall likelihood of project completion. This is an issue that deserves far more open discussion. As argued in my earlier TXF article on the subject, environmental and social due diligence in ECA financings has in some cases become disproportionate, to the point that it risks undermining delivery rather than improving sustainability.

My forecast is that, before long, we will see all ECAs competing more actively for the loyalty and hearts of international SMEs using exactly these kinds of tools. Those that fail to adapt will be left behind.