Global commodity finance 2017: A shift in structure

The TXF commodity finance report has revealed a year-on-year rise in global volumes from 2016. With Middle Eastern traders turning up the heat, Russian producers looking beyond structured trade, and a decline in the usage of PXFs, the findings will surprise.

Global commodity finance volumes have risen to £145 billion in 2017, up from $134 billion in 2016, according to TXF’s Commodity Finance Data Report for 2017.

While there was an increase in structured commodity finance (SCF) year-on-year, spurred by the continued revival of key producing regions such as Russia and the Commonwealth of Independent States, the usage of PXFs and pre-payments declined compared to 2016. However, borrowing base facilities, reserve based lending, and bond financings all increased in 2017.

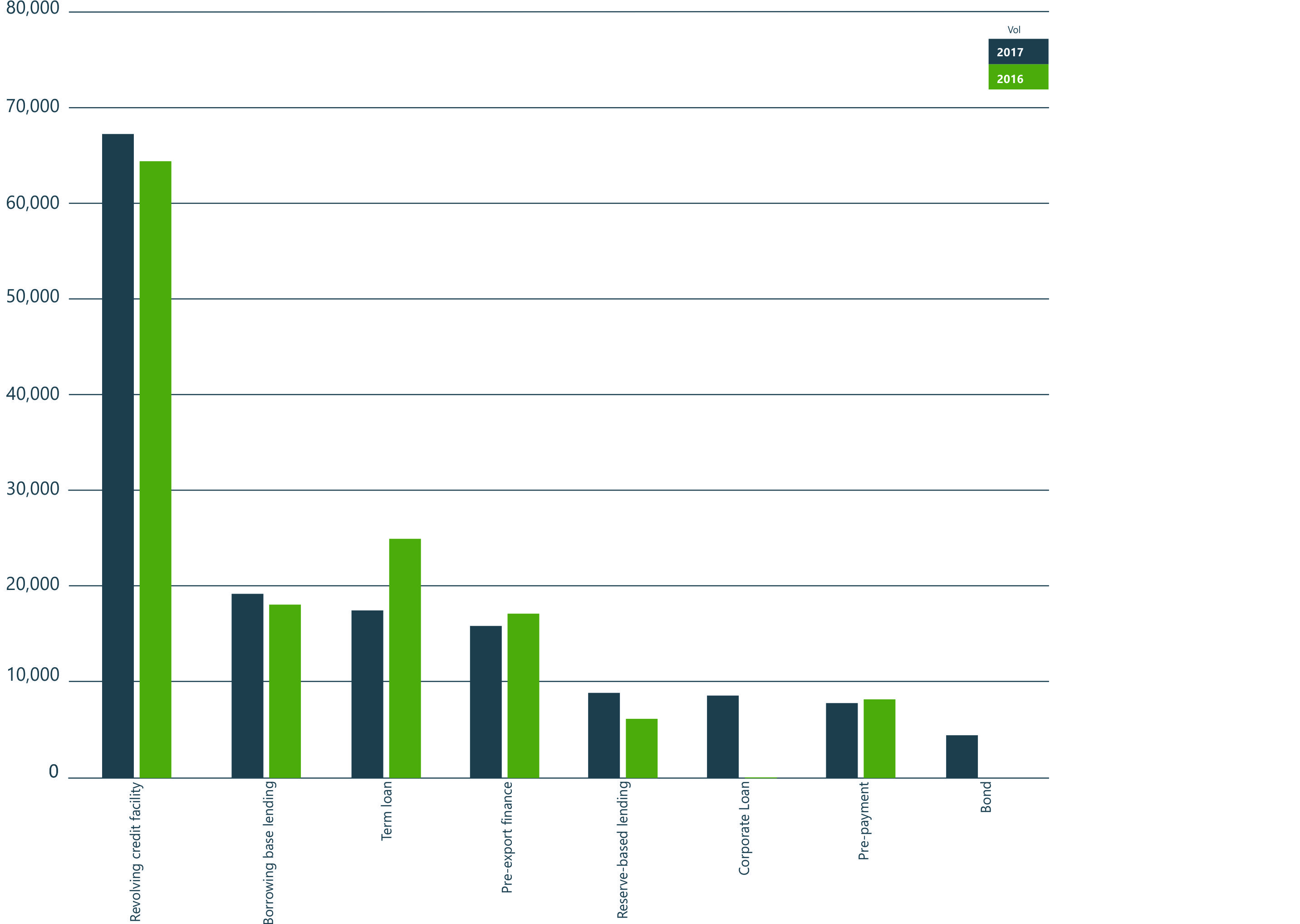

Revolving credit facilities remained the most used facility in 2017 covering 45.5 % of the market, which was in line with 2016’s figures. Traders signed a total of 45 RCFs in 2017, eight more deals than in the same period of 2016, while total volumes remained the same.

Total volume of commodity finance deals in 2017:

It comes as no surprise that unsecured loans comprised nearly 70% of all debts in 2017. And, as Russian corporates continue to re-evaluate their funding mix following a spate of post-sanctions unsecured loan firsts used to refinance secured PXF deals in 2017, corporates in the region are starting to look beyond structured trade financing in a bid to lower their cost of debt and loosen covenants.

The growth of unsecured debt has not been restricted to corporate loans either, with bonds now becoming an increasingly attractive option to borrowers. For example, in July 2017 Eurochem marked its return to the international bond market with a new four-year $500 million Eurobond offering at 3.95%. Likewise, metals producer NLMK is thought to be among those borrowers currently revising their preferred funding structures, with bonds high among the options being considered.

Borrowing bases continued to be the most heavily utilised in 2017 and remained the most used form of SCF. However, the structure is changing and lenders may well be more cautious in the future as terms loosen when they would prefer them to be tighter.

The Russian bear awakens

2017 marked to continued resurgence of Russia and CIS in the commodities space. Russia CIS commodity producers were the most active recipients of bank debt in 2017.

Europeans producers followed closely with $14.2 billion in 2017. While the size of Russian CIS facilities remained the same in terms of volume compared to 2016, deal flow increased marginally by seven transactions. Meanwhile, metals and mining volumes increased in the region more than 60% year-on-year, while oil and gas decreased by $6.5 billion (78%) compared to 2016. In fact, the majority of these facilities in 2016, $12.7 billion, were for producers in the oil and gas and metals and mining sector, which accounted for 24% of the whole producers market.

European traders remained strong in oil and gas in 2017, Africa saw traders debt decrease by 85% in 2017 compared to 2016, and Middle Eastern traders also saw a spike in dealflow by 90% compared to 2016 – which is in part due to one transaction with commodity producer Abu National Oil Company (ANOC) which totalled $6 billion.

Asia-Pacific was the third biggest region for traders bank debt with 19.2% ($15 billion) – representing a $1 billion increase on 2015’s debt. The region was kept out of second place for the second year running despite the increase following a huge year of trader debt in North America. This is partly due to the emergence of the US as a location for large working capital financings for commodity traders.

Deals such as Gunvor USA’s $875 million borrowing base, Mercuria’s $2.1 billion borrowing base, and Antero Resources $4.5 billion borrowing have helped grow the region to $17.7 billion in total financing debt in 2017, though the region is still some way behind Europe on $41.7 billion.

TXF will be examining these trends at TXF Amsterdam 2018, its flagship conference for the commodity finance and natural resources industry. For more information click here.

The full Commodity Finance 2017 report is only available to subscribers. Non-subscribers interested in receiving a copy of the report please email subscriptions@txfmedia.com